In my November 2nd column, I questioned how self-appraised real estate investments purchased by public pensions, like the San Francisco Employees’ Retirement System (SFERS), had appreciated in value, while at the same time comparable investments that are appraised (graded) by the stock exchanges in milliseconds experienced significant declines in value.

As the stock markets have become more volatile, independent financial advisors and firms such as Wells Fargo Advisors, pushed naïve individual investors into a private version of a Blackstone real estate product that SFERS has invested extensively in. In a recent Wall Street Journal article, Carol Ryan coincidentally used my exact November 2nd analogy on the unlikeliness that two identical adjacent houses could having widely different asking prices. Ryan cited that Blackstone had reported to their individual retail investors that they had generated an 8.4% return for the first three quarters of 2022. During that same period, publicly traded real estate funds [1] suffered a 25% loss. Why the disparity?

In the final quarter of 2022, individual investors were dealt a rude lesson on the real value of Blackstone’s real estateproduct when they were not allowed to cash out of these investments. The issue to city employees and taxpayers is what does this portend for the $800 million SFERS has invested in Blackstone products and specifically the approximate $400 million it has invested in Blackstone’s domestic real estate funds?

The two methods Blackstone uses to prop up its value in a declining market

Self-appraising:

Consider the situation of a classroom where a teacher grades students’ tests but allows one set of students to grade their own exams. Should we be surprised that the self-grading students all achieved “A’s,” while the teacher-graded students received “C’s?” This is how Blackstone relays the guesstimated values of their investments to SFERS and to individual investors- straight A’s…. a 4.0 GPA- while parallel investments that trade on stock exchanges earn “C’s.”

Illiquidity- the non-transferability of investment shares:

If an individual wants to liquidate their Blackstone investment, they generally have to sell their investment back to Blackstone. This non-transferability of investors’ interests artificially inflates Blackstone’s guestimated value in two ways:

1) Because there is no public discovery on the prices exchanged between buyers and sellers, it makes it impossible for pensions or individual investors to verify Blackstone’s guestimated values,

2) Blackstone limits the number of redemptions that their customers can liquidate at any time. Thus, only a sprinkling of investors in Blackstone’s products can exit at any time, which prevents a crypto-type run that would expose the true value of the investments.

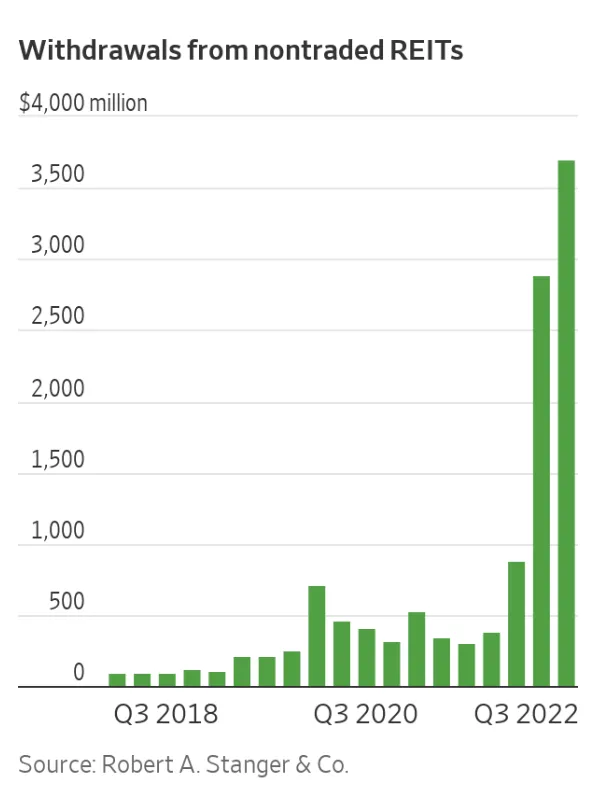

In the fourth quarter of 2022, as reported by the Wall Street Journal, Barron’s, The Financial Times, and Bloomberg, too many individual investors tried to liquidate their Blackstone real estate investments. That forced Blackstone to limit liquidations (called “gating”) of investors’ access to their money. It is this gating on this mini-crypto-type run on Blackstone’s real estate that blinds investors to the true performance of their Blackstone investments.

Because of the run on Blackstone’s real estate investments, on January 3rd, UC Berkeley agreed to invest $4 billion in the same Blackstone investments that individual investors are trying to exit. Per the Wall Street Journal, UC Berkeley, “will be subject to the same fees and terms the other vehicle’s other (individual) shareholders get.” Essentially, UC Berkeley’s is paying the same ridiculously high fees as individuals, without achieving an institutional volume discount. This is neither an endorsement of UC Berkeley’s fiduciary’s skills, nor the self-graded appraisals Blackstone is conveying to individuals and SFERS. But to UC Berkeley, who cares- it’s other people’s money.

Ironically, as individual investors’ have been ramping up their exodus from Blackstone’s real estate investments, as recently as last July, SFERS added another $115 million to the Blackstone Real Estate Partners X.

SFERS opts for the investments that reward the independent contractors with the most money

Funds such as Blackstone generally charge a 2% annual fee on the value of the investment, plus they take 20% of the guestimated profits. Blackstone’s 20% take of SFERS’ profits also incentivizes Blackstone to inflate their guestimated success of the underlying real estate’s appreciation. In this environment, if a Blackstone’s guestimates that their real estate fund generated a 10% return on a $100 million investment, SFERS keeps only $6 million for the pension though accepting all of the investment risk, while Blackstone reaps approximately $4 million, without subjecting their own capital to investment risk.

Why public pension funds’ fiduciaries consistently use public employees’ and taxpayers’ dollars to seek the most expensive products for public pensions, is actually quite simple. Firms such as Blackstone purchase sway by acting as one of the largest donors to politicians, PAC’s, and propositions. From the 2018 two-year election cycle to the 2020 and 2022 elections, Blackstone doubled their political contributions to over $40 million per election cycle.

But before you think it is the just Blackstone’s executives that are buying influence, think again. As exposed by David Sirota in 2018, Blackstone took funds from the actual investments that are in SFERS’ pension and donated to a California statewide proposition. Let me reword that: Blackstone took taxpayers’ and public employees’ money and made political contributions without regards to whether public employees were for or against the proposition. A slippery slope politically and a slimy carousel of money flowing- even if you agree with the side of the proposition Blackstone took.

But don’t worry San Francisco, to oversee this opaque and expensive circus: SFERS conducted a nationwide search to hire a CEO-CIO who doesn’t even have the minimum post graduate degree or a Chartered Financial Analyst license, yet she will become the highest-paid SF public employee with a salary almost doubling the mayor’s. What could go possibly go wrong? This is completely consistent with Bloomberg’s recent article analyzing that the $4 trillion public pension market is being managed by people with inadequate investment expertise.

What should individual investors do?

If you think I am being an alarmist, please listen to Warren Buffett’s recent take on how public pension plans are being taken on the costs, structure, and accounting for alternative investments in pension plans. He called this a one-sided deal that only benefits the product salespersons.

If you are an individual investor and have been pitched a Blackstone-type product like SFERS invests in, don’t walk……run away. Or just follow Warren Buffett’s advice that “really successful people say no to almost everything.’

[1] Technically a Real Estate Investment Trust (REIT)