Writer’s note: I was quoted and a portion of my subject matter from this article later appeared in the Wall Street Journal. Though my article is more about the psychology of taking taking “in-kind distributions” from an IRA at depressed share prices, and marrying those withdrawals to filling up lower tax brackets (24% bracket) with larger IRA distributions. My article is not exclusive to mandatory distributions and is applicable to anyone over 59 1/2 years of age with a large IRA.

Though the markets rallied briefly at the beginning of summer, looking at one’s financial statements in 2022 has not been a pleasant task. For most Americans, the bulk of those statements represented 401k or IRA- type[1] investments, as only about 35% of domestic investors own stocks or bonds outside of those vehicles.

Here are three tax/investment perspectives that retirees should consider when managing their retirement and non-retirement accounts:

- Before accessing or moving funds, categorize investments into three types of tax-vehicle buckets, and prioritize which buckets are the most tax advantageous,

- Know your income tax bracket so you can time your retirement account distributions in a lower tax bracket, and

- Take advantage of depressed stock, bond, and mutual fund prices to take in kind distributions from Traditional 401k’s or IRA’s.

1) Think of tax-vehicle as buckets before you choose which ones to access

CPA’s and financial advisors view assets more distinctly than most investors, cataloguing them into three general tax-vehicle buckets:

- Non-retirement assets held outside of a 401k/IRA,

- Roth 401k/IRA (Whereby your money going in did not create a tax deduction.)

- Traditional 401k/IRA (Whereby your money going in created a tax deduction.)

Each of these buckets create unique tax consequences when money is later moved. Non-retirement assets provide the most flexibility, while at the other end of the spectrum, Traditional 401k’s/IRA’s create the severest inevitable tax consequences. Withdrawing funds from a Traditional 401k or IRA pretty much replicates the same taxable event as if the owner went out and earned that distribution as wages. A distribution from one of these accounts might even bump the taxpayer into a higher tax bracket.

CPA’s and financial advisors differ on which bucket is the most advantageous to access money from. CPA’s generally prioritize that funds should first be removed from Traditional 401k’s or IRA’s, which is in contrast to financial advisors who are often reluctant to recommend withdrawing from these accounts because it affects their compensation.

Whereas a CPA is compensated on an hourly basis[2], most financial advisors are compensated based on a percentage of their clients’ assets held under management (called “AUM.”) As an example, well-advertised, Fisher Investments charges 1.25% on clients’ assets up to $1 million and though Wells Fargo Advisor can negotiate fees lower, their fees are even higher.[3] Thus, a client’s withdrawal from a Traditional account reduces the financial advisor’s AUM, and therefore his income. I am not asserting that that advisors at Fisher or Wells Fargo steer their clients away from removing funds from their Traditional accounts despite the tax advantages, but a potential conflict of interest does exist. It is too easy for financial advisors to rely on rationalizing that a tax delayed is a tax consequence avoided, and retirees frequently lose out on beneficial tax planning.

Consider that with a Traditional 401k/IRA, either the taxpayer or his heirs are going to have to pay that onerous tax eventually, and frequently the most viable solution is to get the tax pain over with now?

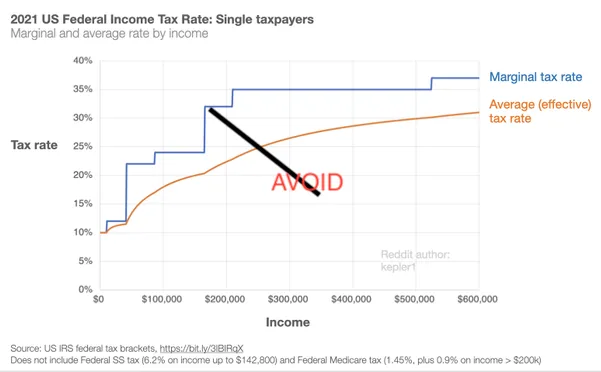

2) Know your tax bracket so you can maximize distributions at lower tax rates

For single retirees, the federal[4] tax bracket on income below $170,000 is 24%. For married couples the same 24% bracket is in effect up to $340,000.[5] Any amount above those thresholds is taxed at a 32% rate—a rate that is 8 percentage points, or 33% higher. Thus, it behooves taxpayers to accelerate distributions to fill in the tax brackets below 32%. Again, either the retiree or his heirs is going to have to pay the tax someday, why not take it at a lower rate.

Example: Suppose a married couple, both 80 years of age, have accumulated $3 million in their IRA. They have $90,000 in income from pensions, interest, and dividends. If they bump their mandatory IRA distribution of approximately $150,000, to $250,000; they will sneak an extra $100,000 out in the 24% tax bracket. The alternative is to let that money continue to grow in the IRA where a portion of it might have to be eventually taken in the higher 32% bracket. The potential federal tax savings on the extra $100,000 is $6,000—a 6% saving–not a bad return.

3) Think of removing companies from your Traditional retirement account, not value

Recently, many commentators have penned articles on how devastating the 2022 market decline has been on retirees’ Traditional 401k’s and IRA’s. Many of these retirees are waiting for stocks or mutual funds in their Traditional accounts to recover to their previous peak prices—so the retiree, then somehow will know the exact time to cash in these stocks, and take a distribution from their IRA. Human nature ensures that when the market recovers, the retirees will not sell and will ride out their investments until the next downturn.

The IRS doesn’t require you to take cash out of your 401k or IRA. You are allowed to take out the actual mutual fund or stock shares (called an “in-kind” distribution.) So, if a retiree is adamant about not throwing in the towel on their investment, they can take distribution of the actual shares.

For example, suppose you own Alphabet (Google) or Amazon directly (or indirectly in a mutual fund). The two companies are down 30% and 48%% respectively from their 2022 high prices. If you still want to hold onto these two companies, you can request that these shares be transferred from your 401k or IRA to your brokerage account.

The bad news is that you will still have to pay tax now on the value of the Alphabet or Amazon shares. But the good news is:

- You will maintain your investment in those companies—and not be throwing in the towel,

- You are removing companies from your Traditional account that you believe are discounted from their future return to their high 2022 share price. Thus, you would be paying tax on a distribution on only 70% of Alphabet or 52% of Amazon from what you would have paid if you cashed out at their peaks in 2022.

- As discussed in the previous section, with an in-kind distribution, you can fill in as much of your 24% tax bracket as possible,

- If you hold onto these companies until you die, any subsequent appreciation, or return to their 2021 high share price, will be tax-free because of the step-up in basis rules. Or you can ignore this IRS tax-free gift, leave your Alphabet or Amazon shares in your Traditional retirement account, and let your heirs pay taxes on that appreciation at a tax rate as if the appreciation was earned through wages—No, please don’t do this!

Note: I specifically cherrypicked Alphabet and Amazon because they do not pay dividends. If you are going to make an in-kind distribution, target stocks or mutual funds that pay little or no dividends, and therefore have no current tax consequences.

Conclusion: You can’t take it with you!

Many financial and tax technicians will read this article and agree that managing tax brackets and taking in-kind distributions is a smart way to strategize one’s retirement account. Many will point out that it would be even better to take these distributions and transfer them to a Roth IRA instead of to a plain brokerage account—and they are correct. However, this article is about perspectives.

Throughout my career of providing financial and tax guidance, I have noticed that investors’ propensity to save is directly correlated to their parents’ proximity to the Great Depression. While most of us didn’t experience that dark financial period, to the extent our parents did, it has affected our savings habits. If you are in your 70’s or 80’s with more than $2 million in a Traditional account, I can guarantee you have applied those same savings habits to have accumulated an additional nest egg in real estate or other non-IRA assets.

Yes, moving money from a Traditional 401k or IRA to a Roth IRA is technically superior, but at the same time, it just locks in that Great Depression mentality of not enjoying life. You can enjoy a richer life, consider taking a vacation with your kids, or help them with a home purchase so your grandchildren will remain close.

Or if you are still worried about outliving your assets, and want to keep your investments intact, consider an in-kind distribution at these depressed stock prices.

Either way, you will survive. You can’t take it with you…. Didn’t I say that already?

[1] 401k/IRA category would also include 403b and 457 Deferred Comp plans

[2] A CPA can wear another hat and operate a financial advisory practice.

[3] Per Lending Trees’ Magnify Money, Wells Fargo Advisors have a “Potential Conflicts of Interest: Since some advisorsmay earn commissions for the sale of securities or insurance products, they may have an incentive to make such recommendations. This creates a potential conflict of interest as advisors may be financially incentivized to make certain recommendations over others.”

[4] California’s tax brackets start climbing at $34,000 for single taxpayers and $70,000 for married couples. As unusual as California is, the Franchise Tax Board (FTB) wants to keep tax brackets confidential. The FTB requires you to request by email what the brackets are. I’m not kidding!

[5] These are 2021 tax rates. The word “tax bracket” does not mean the taxpayer paid a 24% on all their income, just a tier of their income.